20 May 2026

Food Prices Tracker: May 2026

By Finlay Hatch

What’s happening to food prices in the UK?

We've been tracking food prices since April 2022 in response to the cost of living crisis. Since then, the price of food has increased by 30.7% according to ONS data. The food inflation rate decreased from 3.7% in the 12 months to April 2026 to 3.0% with current overall inflation also at 3.0% (CPIH).

While food inflation has yet to accelerate in the way that we expect it to in the coming months, inflation remains above 2% and ever higher prices continue to make it harder for people to afford the food they need each week.

The Food Foundation’s Basic Basket tracking the cost of a weekly shop has seen the cost of the woman’s basket of food now costs £53.51 per week, with the male basket costing £60.24 per week, an increase since April 2022 of 30.6% and 38.4% respectively. To find out more about the Basic Basket, please click here.

The Iran crisis is set to drive up food prices

The Food and Drink Federation has updated its food inflation forecast from 3% to over 9% by the end of the year because of the impact of the war in Iran, and the closure of the Strait of Hormuz. But why exactly does a conflict in a part of the world not well-known for its food production mean people in the UK have to pay more for a loaf of bread?

The last rapid increase in food prices, in 2022, was also driven in part by global conflict. The difference is that Russia’s war in Ukraine destroyed farmland preventing actual food from being produced, removing it from the global market and driving up the price.

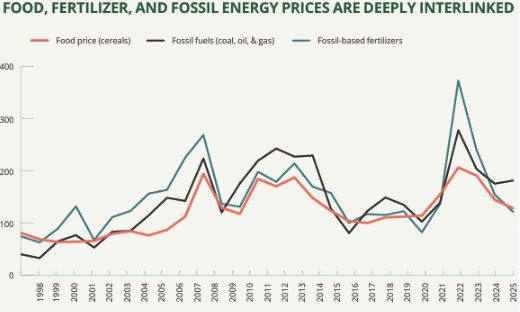

This time, food prices will be driven up indirectly by fossil fuel price rises, revealing how fossil fuels are intertwined in every part of the global food system.

Source: IPES-Food Fuel to Fork report

We use fossil fuels to drive the machinery and create the fertiliser that’s used in farms, and drive the trucks and cool the fridges that allow us to ship food from around the world to the UK. It’s a complex system that means it’s important to understand not only the broad link between fossil fuel prices and food prices, but exactly how each part of the food system will be impacted, and how long it might take for these impacts to filter down to supermarket shelves.

While there is no way to know exactly when each impact will land, especially with the crisis by no means over, there are some clear expectations that experts have for when and why prices might increase throughout 2026.

Transport has already been hit by diesel price hikes

The conflict has slowed the extraction of oil and liquid natural gas and the production of hydrocarbon products across the middle east and stopped their trade from passing through the Strait of Hormuz. While this supply shock has caused the prices of all of fossil fuels to go up, the price of diesel tends to go up first and fastest.

Diesel is the fuel of trade and industry, which can’t respond to price changes as easily as consumers. Ships, trucks, trains and machinery still need to make deliveries and fulfil contracts and so can’t wind down activity in the way that someone commuting to work could choose to ride their bike instead of driving their petrol car.

If demand can’t respond to higher prices, then prices only go up further and faster. This hike has already reached the pumps and will be being factored into food prices already.

Manufacturing, refrigeration and packaging are protected by fixed term energy contracts, for now…

Higher energy costs don’t only impact transport - the organisations and processes that make up the rest of the food chain - manufacturing, packaging, cooling and cooking, are highly energy intensive and all will feel the pinch of higher energy costs.

Small business will already be paying these higher prices, however larger organisations who operate with fixed-term energy tariffs will still paying the same rate as they were before the war. These larger organisations are the price drivers. However, as current contracts expire and large organisations start having to pay higher rates, this cost may be passed through to consumers.

Increased production and supply chain costs will land differently depending on the food item. Energy intensive products such as meat and dairy, processed foods, frozen foods and greenhouse grown fruit and veg will likely become more costly, while domestically grown field crops, perennial fruit and legumes may be more resilient due to their lower fertiliser use.

How has the conflict impacted fertilisers, and farmers?

Fossil fuels are a key ingredient, or ‘chemical feedstock’ of nitrogen, phosphate and sulphur (synthetic) fertilisers. Moreover, the process for manufacturing synthetic fertilisers is incredibly energy intensive, meaning fossil fuels are required both to power the process and as a chemical input to the process itself.

For example, the ‘Haber-Bosch Process’ - the process of turning liquid natural gas into ammonia and then to Urea - the most widely used synthetic fertiliser in the world - is among the most energy intensive process in the chemical industry.

This dual role of fossil fuels in manufacturing fertilisers is why 1/3 of the global trade and so much of the global supply comes from the middle east, a major export region for fossil fuels. The higher fertiliser costs are borne by farmers, and this can change their behaviour in various ways.

- Farmers pay more for scarce fertiliser (pricing out small scale/farmers from lower income countries) and pass costs down the supply chain to consumers.

- Farmers reduce fertiliser use and face lower yields or plant fewer crops, reducing food supply, driving up prices and risking empty shelves.

- Farmers exit the marketplace altogether, again reducing supply, causing higher prices and risking empty shelves.

What does this mean for consumers?

The common theme is that the drop in supply and/or higher prices will not hit consumers immediately. In the UK, most fertiliser for this year’s application will likely already have been bought and applied by the time the crisis hit, and there are reports farmers are waiting to see if prices fall before buying more.

But if prices remain high, the impacts will only start to be felt towards the end of this year as the lack of fertiliser hits imported goods, and into next year as British farmers start to either pay more or risk lower yields.

It’s clear that the crisis has already locked in medium term consumer food price increases, but exactly how acute the crisis turns out to be depends on several factors that remain uncertain.

Some experts believe that the global food system is in a better place to deal with a food system crisis than 2021/22, with a bumper global harvest expected this year and macro-economic indicators in a more favourable place.

Others, including farmers themselves, point out that this spells trouble for farmers, squeezed in between higher input costs for next year's crops and lower prices this summer.

What’s more, for consumers, this shock comes on the back of a period of food price increases unprecedented in recent decades - it’s expected that by the end of 2026, food prices will by 50% higher than they were in 2021, a rate of increase in 4.5 years that had previously taken over 19 years.

The six million households still living in food insecurity can scarcely afford another cost of living crisis.

- If you’d like to be kept informed as the situation develops please sign up to our newsletter.