18 November 2021

Food Prices Tracking: November Update

by Shona Goudie and Rebecca Tobi

Food price inflation over recent months is an area of growing concern. In this blog we look at what has happened to food prices in the past month and what we might expect to happen next.

What has happened to inflation over the past month?

Government data from the latest Consumer Price Index (CPI) release reported that in October 2021, the CPI rose by 4.2% in the 12 months to October 2021, up from 3.1% in the 12 months to September. On a monthly basis the CPI increased by 1.1% in October 2021 compared to the preceding month.

What has happened to food prices over the past month?

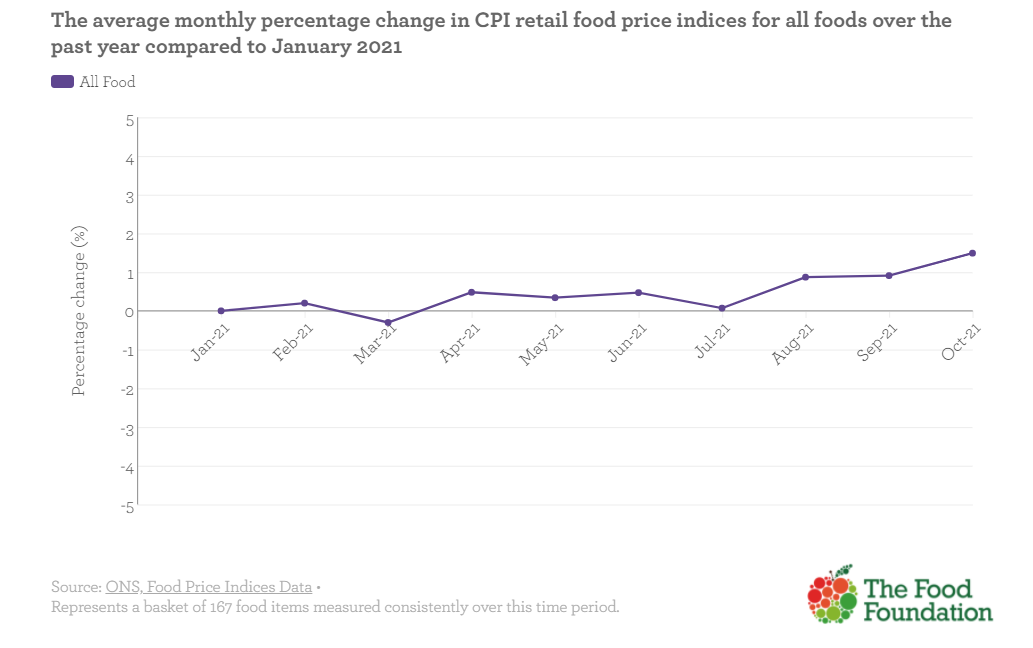

UK Food Prices

Looking only at the CPI food retail basket, Food Foundation analysis shows that inflation increased by 1.95% in October 2021 compared to January 2020 (pre-pandemic) and was 1.49% higher than at the beginning of this year in January 2021. Compared to last month, the retail food price index rose by 0.54%.

As a point of comparison, Kantar reported that like-for-like grocery price inflation in the four weeks to mid-November reached 2.1% - rising at the fastest pace since August 2020. This has largely been attributed to supply chain issues, with demand outstripping supply. Kantar data indicates that savoury snacks, canned coke and crisps are amongst the highest rising food prices whereas prices fell for bacon and vegetables1. Nielsen have said that the price of seasonal fresh foods are helping to offset the increase in prices of shelf-stable and tinned products2. In real-world terms, in October, Kantar reported that the average household had to spend an additional £5.94 on food in the last month compared with the same time in 20203.

Within the CPI retail basket certain food products and categories have been more affected than others. The index rose by 0.92% for starchy staples (foods that comprise the majority of the diet for most people, such as rice, bread, and potatoes) compared to the start of this year. Inflation increased by 11.3% for a packet of pasta compared to the start of the year, and by 5.7% for a large loaf of bread. As a category, inflation also increased for meat, likely as a result of labour and supply chain pressures. Inflation was 1.9% higher for fresh chicken and 10.7% higher for a shoulder of lamb. Fruit and vegetables, both key components of a healthy diet, remained higher in price than before the pandemic, with fruit increasing by 1.55% in October compared to September.

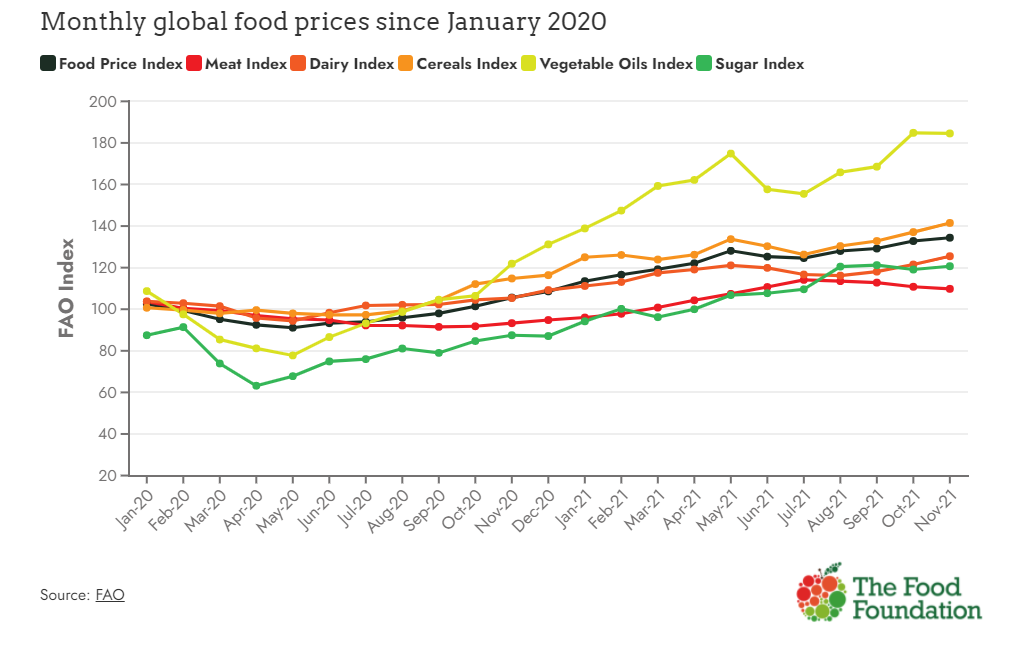

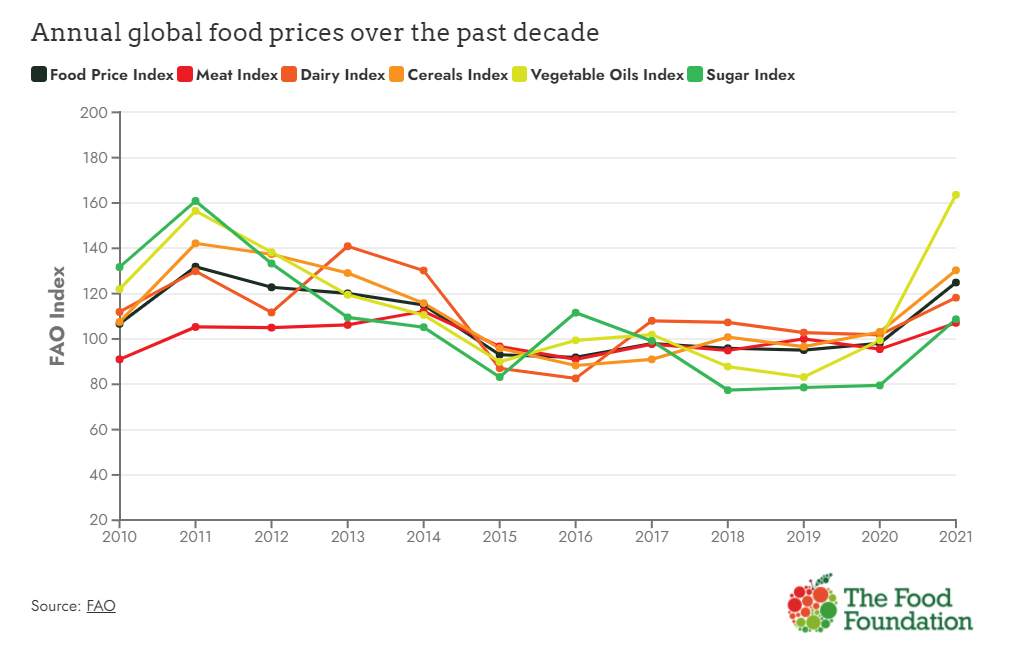

Global Food Prices

Globally, world food prices are soaring. In October, the Food and Agriculture’s (FAO) Food Price Index reached its highest level since July 2011. In October 2021, the FAO Food Price Index was up 3.9 points (3.0 percent) from September and 31.8 points (31.3 percent) from October 20204.

The rise in food prices globally is in large part due to increases in the price of cereals and vegetable oils, with the former an important part of staple diets in low and middle income countries. Cereal prices are now 21% higher than they were this time last year in October 2020.

What could happen next?

UK inflation is rapidly increasing and forecast to continue doing so

Overall inflation is currently at 4.2%, ahead of the Bank of England’s 2% target5. They have predicted that it will continue to rise in the coming months, peaking at the highest level in almost a decade in April 2022 at 5%6. But it is difficult to predict to what extent food price inflation will mirror this and whether it will result in increased food prices passed through to citizens. Although so far, the CPI food retail index has risen more slowly than overall inflation, the higher levels of food inflation seen in recent months merit concern about an upward trend. Overall inflation may also put pressure on food budgets of low-income families if this inflation is not translated into increases in wages.

Supermarkets are assuring customers they will keep prices down

Interestingly, although many wholesalers and retailers would usually bear the brunt of any price fluctuations themselves rather than passing these onto consumers, we can see from CPI and Kantar data that supply chain pressures are such that companies are starting to increase the retail prices of certain products. This is in keeping with reports from large manufacturers including Unilever (maker of household brand names such as Marmite and PG Tips) and Nestle who confirmed that they will be increasing the price citizens pay for their products7. Similarly, the hospitality sector are saying they will most likely have to increase prices8.

However, Sainsburys Chief Executive recently assured customers that while they were unable to predict food prices they are committed to keep them at a minimum9, with Tesco doing similarly10. This is despite CPI and Kantar indicating that customers are already facing higher prices, and a survey by the British Retail Consortium indicating that three in five retailers expect prices to increase leading up Christmas11.

In the face of continued food shortages, retailers may employ such tactics as reducing promotions as was seen at the start of the pandemic12,13. There is also likely to continue to be a decrease in the choice of products available14, and there may also be decreases in the size of products sold, known as shrinkflation15.

Government attempts to address the issues are unlikely to be enough to keep prices down

The BEIS16 and EFRA17 parliamentary select committees have been hearing evidence over the past month on labour shortages and disruption in the food supply chain. But so far, Government has done little to mitigate increases in food prices and shortages. Their main strategy has been to help tackle labour shortages by making additional temporary visas available for 5,500 poultry workers, 800 pork butchers and 4,700 HGV food drivers18. However, Britain’s Road Haulage Association say there is a shortage of 100,000 drivers19 and Government told the Transport Select Committee that the HGV driver issues will last until at least the end of 202220. They have introduced a slaughter incentive scheme to specifically support the issues in the pig industry21. Given the scale of the problem, these measures are unlikely to sufficiently curb the many factors contributing to increases in food prices.

Conclusion

Predictions are that we will most likely see food prices continuing to rise in the coming months as we increasingly feel the effects of labour and food shortages, and manufacturers and retailers struggle to absorb the costs. We will continue to monitor the situation with food prices over the coming months, as well as the subsequent impact on food insecurity for low-income households.

Food more information on food prices see our Food Price Tracker and our blog on why food prices are rising.

Shona joined The Food Foundation as a Project Officer in 2019 and has worked on research, policy and advocacy across a range of projects over that time including leading our food insecurity surveys and flagship annual Broken Plate reports. She now works across the charity's policy portfolio including our children's food campaigns, food insecurity and food environments. She is a Registered Associate Nutritionist with a background in clinical nutrition who worked in dietetic departments in NHS hospitals before joining The Food Foundation.

Rebecca joined the Food Foundation in January 2020, leading on the Peas Please initiative. These days she manages our business and investor engagement team, with oversight of our work engaging food businesses, investors and policy-makers with the need to transition the UK towards a more sustainable and healthy food system. This includes our Peas Please and Plating Up Progress projects.

Rebecca is a Registered Nutritionist (RNutr) with a background in science communication, joining the Food Foundation from the Nutrition Society. In a previous life, Rebecca worked in the marketing and tech sectors before deciding to move into nutrition, obtaining a MSc in Nutrition for Global Health at the London School of Hygiene and Medicine.

Rebecca is a lover of veg (peas really are her favourite vegetable), a staunch advocate for evidence-based nutrition communication, and is passionate about structural changes that make healthy and sustainable diets accessible for all.